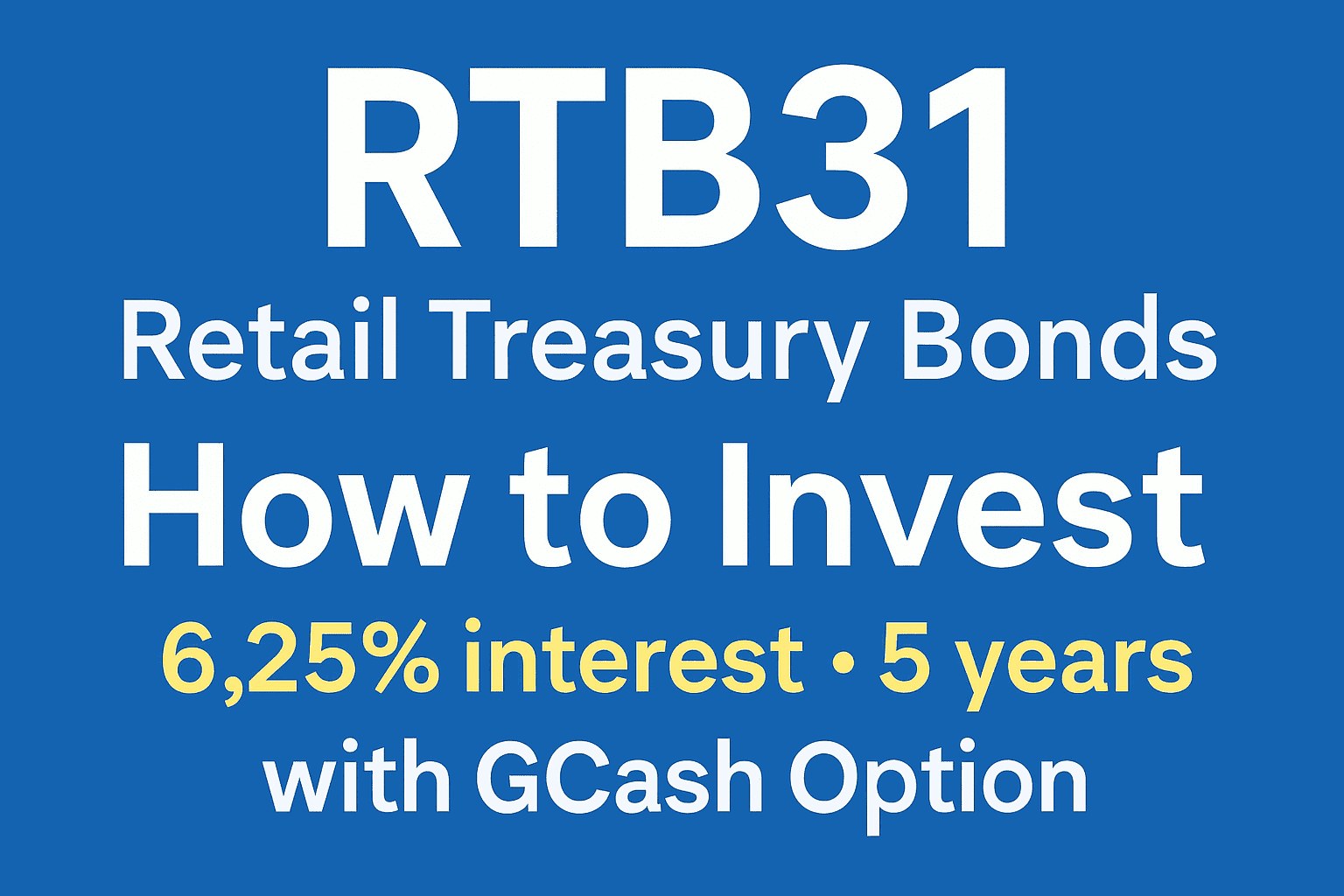

Update as of August 17, 2025:RTB 31 is no longer available for purchase. The public offering ran from August 5 to August 15, 2025, and the Bureau of the Treasury has since closed subscriptions for individual investors. While you can … Continue reading

How to Invest in RTB31 (Retail Treasury Bonds) — Full Guide for Filipinos

2