Pag-IBIG Fund has officially announced the dividend rates for 2025 — and once again, members are getting strong, tax-free returns.

If you’re contributing to Pag-IBIG Regular Savings or investing in MP2, here are the confirmed numbers you need to know.

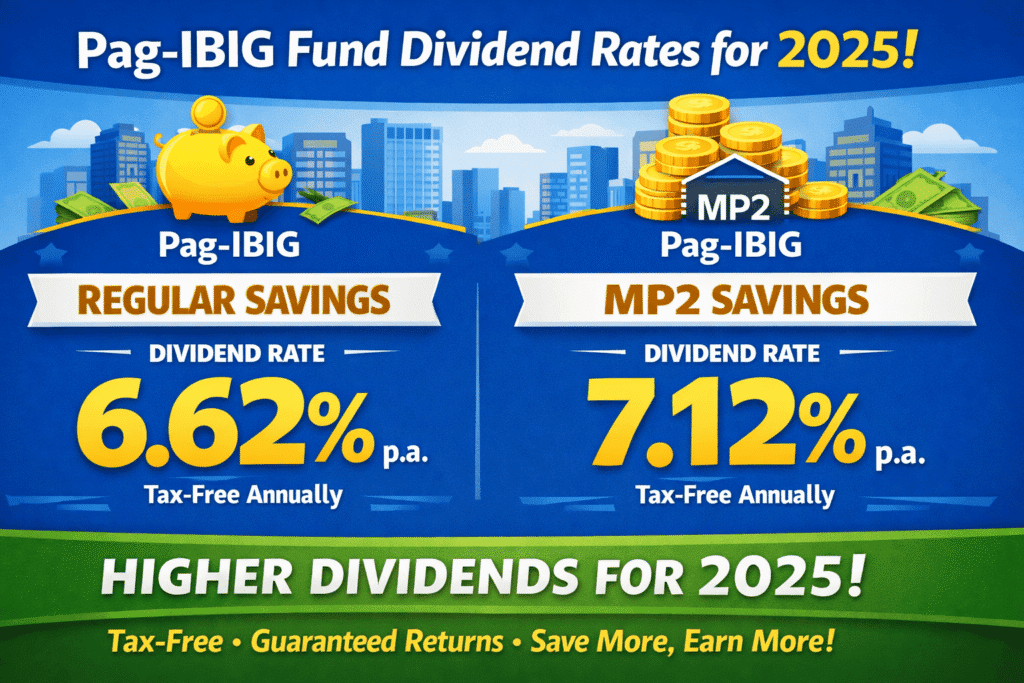

Official Pag-IBIG Dividend Rates for 2025

For the dividend year 2025 (to be credited in 2026):

- Regular Savings Dividend Rate: 6.62% per annum

- MP2 Savings Dividend Rate: 7.12% per annum

Both are annual and tax-free.

That means whatever dividend you earn goes directly to your account — no withholding tax, no deductions.

What These Rates Mean for Members

Pag-IBIG is required by law to return at least 70% of its annual net income to members in the form of dividends. Because of strong investment performance in 2025, the Fund was able to declare slightly higher rates compared to the previous year.

For comparison:

- 2024 Regular Savings: 6.60%

- 2024 MP2: 7.10%

- 2025 Regular Savings: 6.62%

- 2025 MP2: 7.12%

While the increase may look small, it makes a big difference when you’re talking about six-figure savings and compounded growth.

Sample Computation (MP2 – 7.12%)

Let’s say you have ₱100,000 in your MP2 account before dividends are credited.

Dividend earned:

₱100,000 × 7.12% = ₱7,120

Your new balance becomes:

₱107,120

If you leave that money invested, next year’s dividend will be computed on the higher amount. That’s the power of compounding.

Now imagine if you’re investing monthly — the long-term growth becomes even more attractive.

Sample Computation (Regular Savings – 6.62%)

For employees contributing the mandatory ₱200 monthly (₱2,400 per year personally, ₱4,800 total including employer share):

If your total accumulated savings for 2025 is ₱50,000:

₱50,000 × 6.62% = ₱3,310 dividend

Again, completely tax-free.

When Will the 2025 Dividends Be Credited?

Pag-IBIG typically credits dividends in the first quarter of the following year.

So the 2025 dividend earnings will be reflected in your account in early 2026. You can check it via Virtual Pag-IBIG once posted.

Why MP2 Continues to Be Popular

The MP2 (Modified Pag-IBIG 2) program remains one of the most attractive low-risk savings options in the Philippines because:

- Higher dividend rate than Regular Savings

- Government-backed

- Tax-free returns

- 5-year maturity

- Flexible contributions (lump sum or monthly)

For conservative investors who want better returns than most traditional bank savings accounts, MP2 continues to stand out.

Is Pag-IBIG Still Worth It in 2026?

With 6.62% for Regular Savings and 7.12% for MP2, Pag-IBIG remains competitive — especially considering:

- No tax on dividends

- Backed by a government institution

- Historically consistent dividend performance

If you’re building long-term savings, planning retirement, or just looking for stable returns, these rates make a strong case for continuing (or starting) your contributions.

Blogger’s Corner

Every year, some people ask: “Is MP2 still worth it?”

When you compare 7.12% tax-free returns versus most savings accounts earning 2% to 4% before tax, the answer is clear for conservative investors.

It’s not a get-rich-quick investment.

But it’s steady.

It’s predictable.

And it compounds quietly in the background.

For long-term Filipino savers, that consistency matters more than hype.

Hello!

I have been a member for several years in Pag-Ibig Fund. I just pay the regular amount of P500 peso monthly in the Philippines.I am an OFW here in Thailand and I always pay monthly the P500.00.

Will you kindly tell or inform me again what are my benefits because I already don’t know the I formation recently in this Pag Ibig Fund. I want to use some of my benefits because I am a single parent or mother that to make my ends meet.

Also, I want my son to benefit from this.

My querries are:

1. Will I receive a retirement pay?

What is the coverage of my retirement and how much will I receive?

2. What are my benefits?

3.Can my son be benefited from this since I wrote his name as my beneficiary,?

4. Can I make a loan though I am here abroad? If so, how much and how is the computation? How many months to pay thiis loan?

5. Can I use my Pag Ibig as my insurance in going for check up and medical health there and here in abroad? Or in the philippines only?

Can my son use my Pag Ibig insurance for health check up and medical bills there in the Philippines?

Looking forward to a favorable response in this matter.

Thank you so .much.

Lihzie

1. Pag-IBIG regular savings is not a pension fund like SSS. Like what the name says it is a savings program where your contributions earn a dividend. Once you reach the retirement age of 60, you can withdraw all your contributions + dividends earned. You can also opt for an early withdrawal if you have at least 240 monthly contributions.

2. More details here: https://poorpinoyinvestor.com/pagibig-regular-savings/

3. In case of death, the beneficiary can claim all the contributions + dividends of the member. And if the member’s account is active by the time of death, the beneficiary can also file a death benefit claim.

4. Refer to this: https://poorpinoyinvestor.com/pag-ibig-mpl-2025-guide/

5. Pag-IBIG regular savings is not an insurance.

My 5-year MP2 PAG-IBIG account matured on January 6, 2026. I withdrew the principal amount on the same date. However, PAG-IBIG has yet to issue the 2025 dividend, which is expected between February and March 2026. Am I still eligible to receive the 2025 dividend for the account I already withdrew?

The dividend for the last year will be based on the most recent dividend rate.